On March 13, 2026, the U.S. Office of Personnel Management Office of Inspector General (OPM-OIG) released an audit report regarding the Federal Employee Health Benefit Plan (FEHBP) administered by Blue Cross Blue Shield (the “Plan”), and more specifically the Plan’s retail and mail-order pharmacy programs administered by CaremarkPCS (“Caremark”). The audit covered contract years 2018 through 2021 and examined administrative fees, annual accounting statements, claims eligibility and pricing, drug manufacturer rebates, the fraud and abuse program, and performance guarantees for FEHBP pharmacy operations.

The OPM-OIG concluded that Caremark caused BCBSA and the FEHBP an astounding $615,148,628 in losses, including lost investment income, by failing to pass through all discounts, credits, and financial benefits related to prescription drug pricing as required under the PBM Transparency Standards found in the Carrier’s contract with OPM.

The Pass-Through Pricing Framework

To understand the audit’s findings, it is essential to understand the two primary drug pricing models used in the PBM industry. The first, known as “traditional” or “spread” pricing, allows the PBM to profit from the difference between what it charges the health plan and what it actually pays the pharmacy, a margin known as “spread.” The second, more modern approach, is known as “pass-through pricing.” Under this model, the PBM’s profit is derived solely from an administrative fee paid by the health plan or plan sponsor, and all discounts, rebates, credits, and other financial benefits negotiated by the PBM with drug suppliers are passed through to the plan.

Since 2011, the PBM Transparency Standards in Section 1.26(a) of OPM’s Contract have explicitly required pass-through transparent pricing, meaning the carrier must receive the value of the PBM’s negotiated discounts, rebates, credits, or other financial benefits. Despite this requirement, the audit uncovered two mechanisms by which Caremark retained financial benefits that should have flowed to the FEHBP.

Finding 1: “Sham” Pass-Through Scheme

The largest finding, totaling $478,717,560 (including $77,977,735 in lost investment income), concerned Caremark’s failure to pass through the discounts it negotiated with two of the largest national retail pharmacy chains. The OPM-OIG found that Caremark reimbursed FEHBP claims at these pharmacies at a lower discount, and therefore a higher price, than the discount rates stated in Caremark’s own retail pharmacy agreements.

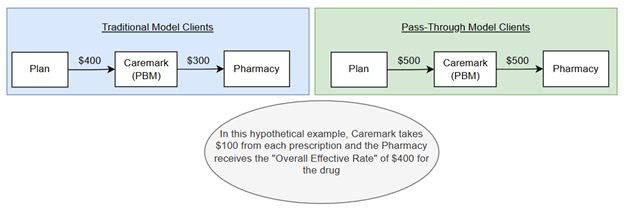

The mechanism was rooted in how Caremark structured its pharmacy agreements. Rather than applying a fixed discount rate to each claim, Caremark’s contracts with these two national pharmacies contained “Overall Effective Rates,” which measured discounts in aggregate across the PBM’s entire book of business, encompassing all of its clients, both government and commercial. This flexibility allowed Caremark to reimburse FEHBP claims at a lower discount (higher cost) while applying more favorable discounts to claims from its traditional “spread” clients, where Caremark could mark up the price and profit from the differential. In effect, the pass-through client (the federal government) subsidized better pricing for Caremark’s traditional commercial clients, enabling Caremark to extract greater spread from those accounts. For example:

Finding 2: Retention of Retail Pharmacy Transmission Fee Credits

The second finding, totaling $108,600,029 (including $16,170,786 in lost investment income), involved Caremark’s collection and retention of per-transaction “transmission fees” from retail pharmacies. Caremark charged these fees to retail pharmacies for use of its electronic claims adjudication system, and the fees were credited back to Caremark by reducing the weekly payments it owed to the pharmacies. However, Caremark continued to bill the carrier and FEHBP at the full, pre-credit claim amount, thereby pocketing the difference.

The OPM-OIG found that Caremark collected $92,429,243 in transmission fees allocable to the carrier’s FEHBP retail claims during the audit period. Because the PBM Transparency Standards required pass-through of all credits, and because the carrier already paid a per-claim administrative fee covering “electronic claims processing and pharmacy reimbursement,” the OIG concluded that these credits should have been passed through to the FEHBP. Caremark argued that transmission fees were unrelated to drug pricing and were instead fees for network administration services, and that OPM did not explicitly require pass-through of transmission fees until the 2024 amendments to the standards. The OIG rejected this defense, noting that the fees functioned as credits that directly reduced the cost paid for drugs, and that the 2011 standards already required pass-through of all credits.

Notably, this is similar to the position PBMs often take with respect to manufacturer administrative fees and other manufacturer-derived payments in connection with formulary rebates. PBMs and their affiliated rebate aggregators argue that such fees are somehow totally unrelated to the rebates earned by the Plan, even though the payments are calculated as a percentage of the value of the drugs utilized by Plan members. The OPM-OIG adds to the body of findings, settlements, and other precedent holding that PBMs cannot promise pass-through of credits and rebates and then not deliver on that promise by merely re-labeling the revenue as unrelated income.

Why This Audit Matters: Lessons for All Plan Sponsors

While the dollar figures alone (more than $615 million in overcharges to a single health plan over just four contract years) are staggering, this audit is notable for a reason that extends well beyond the FEHBP. It demonstrates, with granular detail, how a large PBM can systematically extract “spread” even under a contract that expressly mandates pass-through transparent pricing. The mechanisms identified in this audit (manipulating variable discount rates across a commingled book of business, retaining undisclosed credits from pharmacies, and clawing back savings through incentive structures) are not unique to government contracts. They are structural features of how large PBMs contract, even with unaffiliated retail pharmacies, and they can be deployed against any plan sponsor.

The core lesson is that negotiating a “pass-through” PBM contract, standing alone, is insufficient to protect a plan sponsor from overcharges, because PBMs can manipulate pharmacy reimbursement rates to the Plan’s detriment. For example, a recent audit conducted by the Tennessee Department of Agriculture reported that Caremark “used reimbursement practices that led to higher payments for prescription medications dispensed at the PBM-affiliated retail, mail order, and specialty pharmacies than payments made to the non-affiliated” pharmacies.[1] By agreeing to pass-through rates, the Plan is effectively agreeing to pay the inflated prices that Caremark is paying to its sister companies. But such profiteering is not limited to PBM-affiliated pharmacies. As this audit revealed, Caremark exploited the flexibility inherent in “Overall Effective Rate” arrangements with non-affiliated retail pharmacies to apply less favorable discounts to FEHBP claims while reserving better discounts for its traditional spread clients.

This finding exposes a fundamental vulnerability in pass-through arrangements: when a PBM negotiates “Overall Effective Rate” discounts with major pharmacy chains on an aggregate, book-of-business basis, it retains discretion over how to allocate those discounts among its various clients. A plan sponsor with a pass-through contract may believe it is receiving the benefit of the PBM’s negotiated rates; but in reality, the PBM may be subsidizing better pricing for its spread clients at the plan sponsor’s expense.

The implications for commercial plan sponsors are clear. A pass-through contract is only as protective as the plan sponsor’s ability to verify that pass-through pricing is actually being delivered. Plan sponsors should insist on robust audit rights that include access to the PBM’s pharmacy agreements and the specific discount rates contained therein, require claim-level reconciliation to the PBM’s negotiated rates, demand disclosure of all fees, credits, and financial benefits the PBM collects from pharmacies, and carefully scrutinize any incentive or shared-savings provisions that could allow the PBM to recapture savings that should flow to the plan. Without these safeguards, the label “pass-through” may provide a false sense of security while the PBM quietly siphons value through the very contract structures that were supposed to ensure transparency.

How Frier Levitt Can Help

Frier Levitt advises health plans, employers, and other plan sponsors on PBM contracting, audit strategy, and pricing transparency. Our team has extensive experience identifying hidden revenue streams, evaluating pass-through arrangements, and enforcing contractual rights through audits, disputes, and litigation. If you are concerned about PBM pricing practices or want to ensure your contract is delivering true pass-through value, contact Frier Levitt to assess your exposure and protect your plan.

[1] https://tnpharm.org/wp-content/uploads/CaremarkReportAuditPackage_20260212.pdf at page 6.

Senior Associate